Bumble’s Billion Dollar Hidden Tax Shield Feeds a 47% FCF Yield

Deep value in the duopoly of online dating $BMBL

Bumble BMBL 0.00%↑ generated free cash flow of $182.4M in the first 9 months of 2025, annualized that is $243.2M. At Bumble’s $454M market cap that is a 53.6% FCF yield, 47.2% after deducting annualized SBC of $28.8M. After repurchasing their tax receivable agreement for $186M Bumble is a business with serviceable net debt of $478.2M and a leverage ratio of 1.78. At this valuation the business is priced for a rapid decline, I don’t believe that’s likely.

Bumble went public using an Up-C structure, an uncommon arrangement that it’s in the middle of unwinding. The added complexity requires a bit more digging which often increases the opportunity that the market is missing something. In this case we have a hidden tax asset and underappreciated forward cash flow. Bumble has two distinct tax assets; traditional NOLs and a massive pool of billions in deferred tax assets that were created through the Up-C structure.

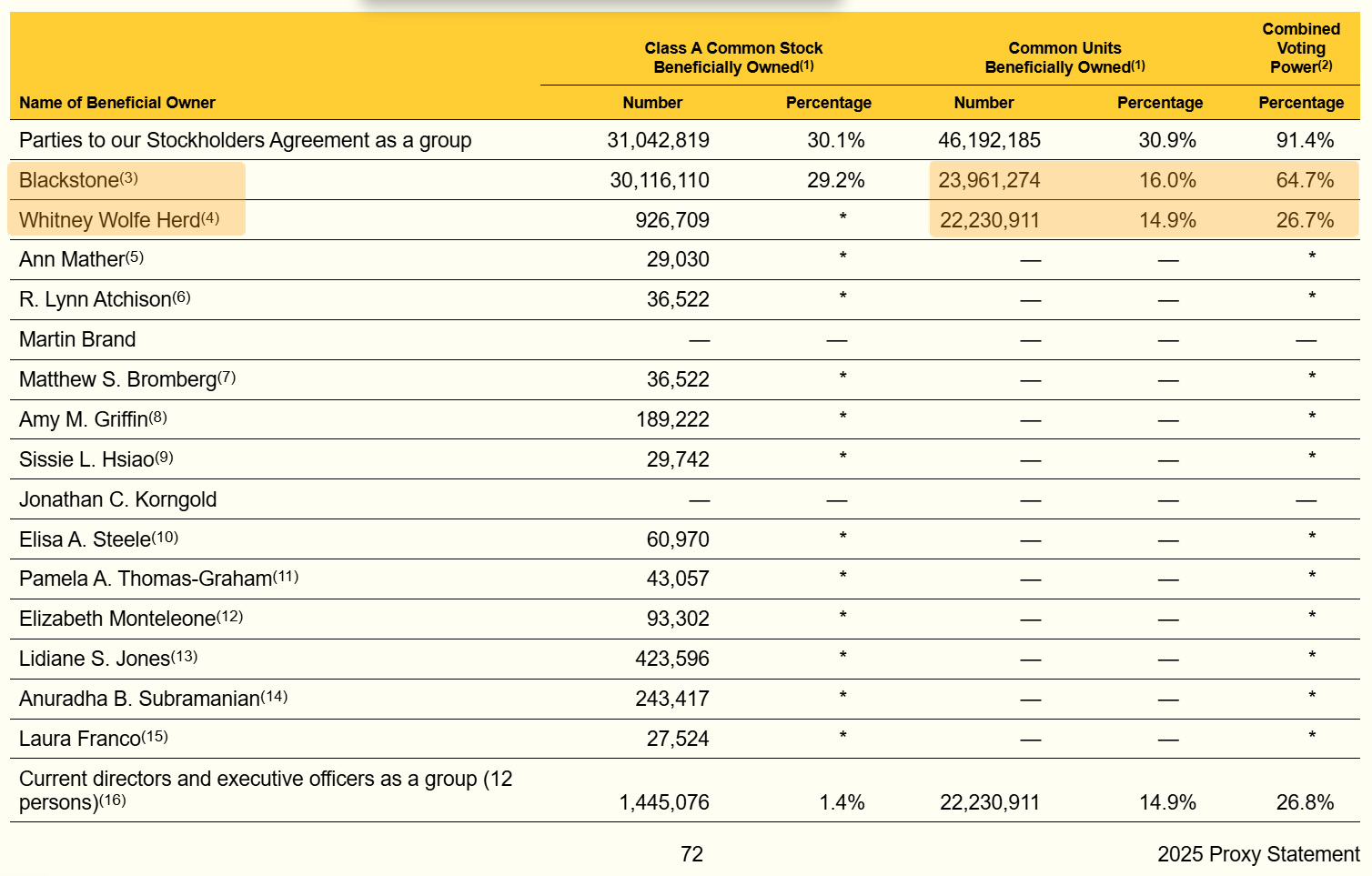

Bumble inc. is the public shell, whereas Buzz Holdings is the private partnership that owns all the assets. A share of the Bumble inc. shell entitles you to a common unit of the private partnership Buzz Holdings. As of Q3 2025 there are 112.7M A-shares of Bumble inc. but the true share count has to include the 37.8M privately held common units of Buzz Holdings which most screeners miss.

In April 2025 Whitney Wolfe and Blackstone were the primary private stakeholders in the partnership with a combined 46,192,185 common units. Whitney then converted and sold 1,000,000 common units in August and Blackstone converted 7,395,159 units and sold them alongside an additional 9M of their pre-existing A-shares. In total Blackstone sold 16,689,884 shares in a block sale for $6.26 per share. This left 37,797,026 common units in the partnership at the end of Q3 and 112,738,975 A-Shares for a true total of 150,536,001 shares outstanding.

In November Blackstone fully exited the buzz holdings partnership and converted their remaining stake into 16,566,115 A-Shares. This greatly increased the public float and left a market overhang that has likely aided in depressing the stock price as the narrative of an insider liquidating plays out and the threat of future sell-off looms.

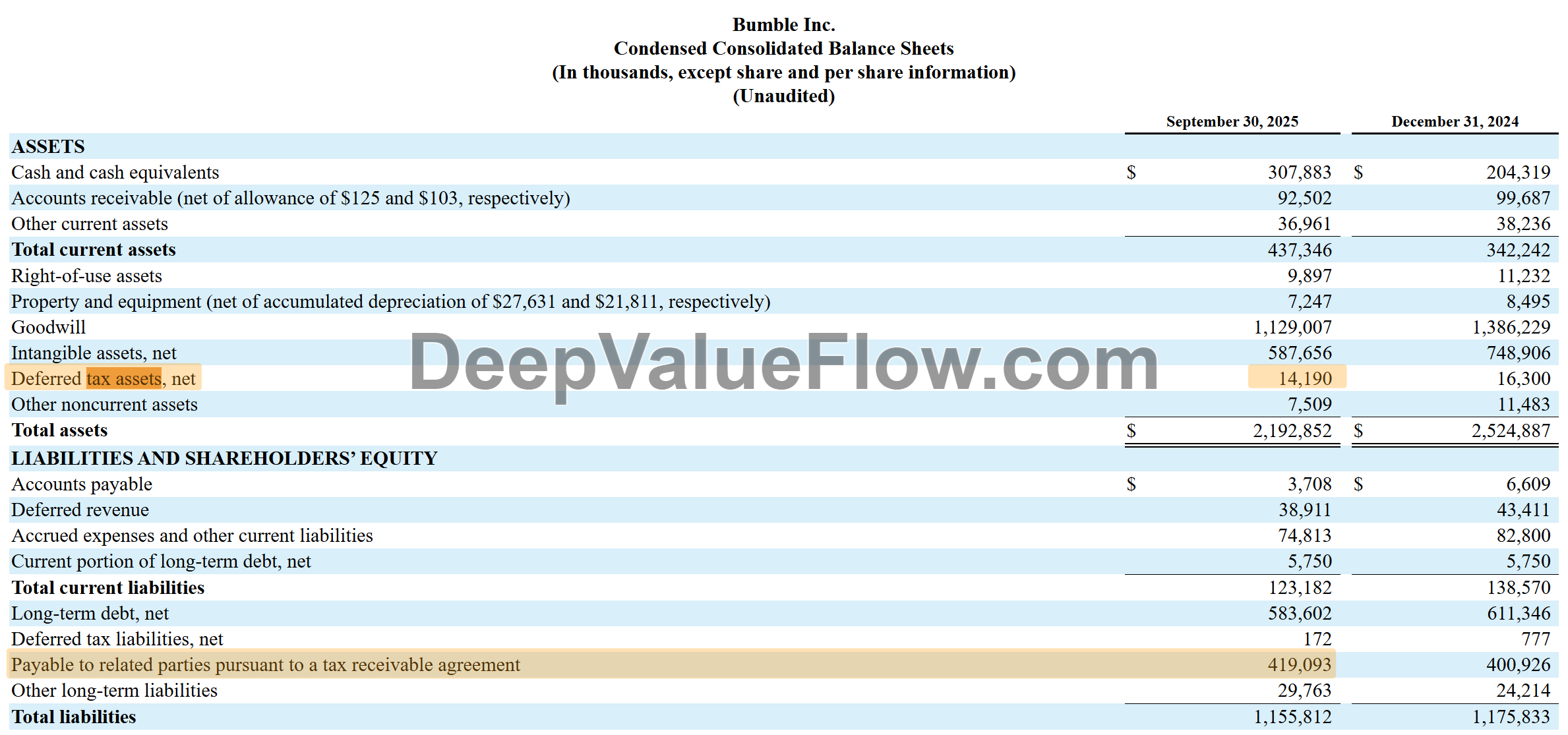

“Based on current projections, the Company anticipates having sufficient taxable income to realize the benefit of this Common Basis and has recorded a tax receivable agreement liability to related parties of $419.1 million related to these benefits as of September 30, 2025.”

Bumble 10-Q (Q3 2025)

In Q3 the company believed they are likely to save $493M in taxes from the banked step-up losses. They go on to say to the extent they can realize additional tax benefits they would record an additional $273.3M liability for a total of $692.4M in potential TRA payments. The DTA could be used to shield 100% of their taxes but the terms of the TRA required 85% of these savings be paid to the pre-IPO parties, primarily Whitney and Blackstone. Since this TRA was repurchased for 186M in Q4 this nearly $700 million in TRA tax savings will be converted on a flat line basis to cash flow over the next 10-15 years. Bumbles deferred tax assets as a whole are potentially worth 814.6M in tax savings which is almost twice the total equity value of the business and far in excess of the 14.19M value they are carried at on their balance sheet.

Unlike NOL which do not expire, these UP-C tax benefits expire within 15 years and that timer starts anytime Buzz Holdings common units are exchanged for Bumble inc. A-shares, as a result the bulk of these DTAs expire in the next 11 years. If we discount the 419.1M - 692.4M value of the repurchased TRA at 10% on a straight line basis over 11 years the conservative present value of the asset is $247.5M - $408.8M. Essentially Bumble got a discount of roughly 25-56% when they paid 186M to buyout this TRA on November 6th. This valuation assumes Bumble can roughly maintain taxable income above ~$90M on the low end and ~$250M on the high end for a decade straight, which may not happen. After stripping away goodwill impairments analysts expect FY 2025 taxable income of $144.4M-$151.4M. The present value estimate of the TRA value doesn’t include subsequent tax asset creation from Whitney Wolfe Herd exchanging her remaining Buzz Holdings for Bumble inc. A-Shares. The value of this exchange is dependent upon the stock price when they are converted and has potential to be quite significant if the stock rebounds in the next few years.

In the end the founders got a lump sum for an asset with a lot of uncertainty and they increased the value of their stake in the underlying business which is now primed for cashflow and ripe for acquisition. Perhaps the CEO will cease to be a net seller of stock and use her portion of this payout to increase her stake in the company. The knock-on effect of clearing this $400M non-interest bearing liability was a S&P ratings upgrade from B to B+ closer to the BB- rating they hold with Fitch. This likely allowed them to knock 50 basis points or more off their debt; a refinance announcement is expected during the Q4 earnings on March 11th.

Evaluating the Underlying Bumble Business

Dating apps are uniquely cyclical. A business of apps analysis from 2025 found that fewer than five percent of monthly subs are still active 12 months later. This makes revenue slightly less dependable than your average SAAS but it also means short term changes in DAU are less dependable predictors of future performance.

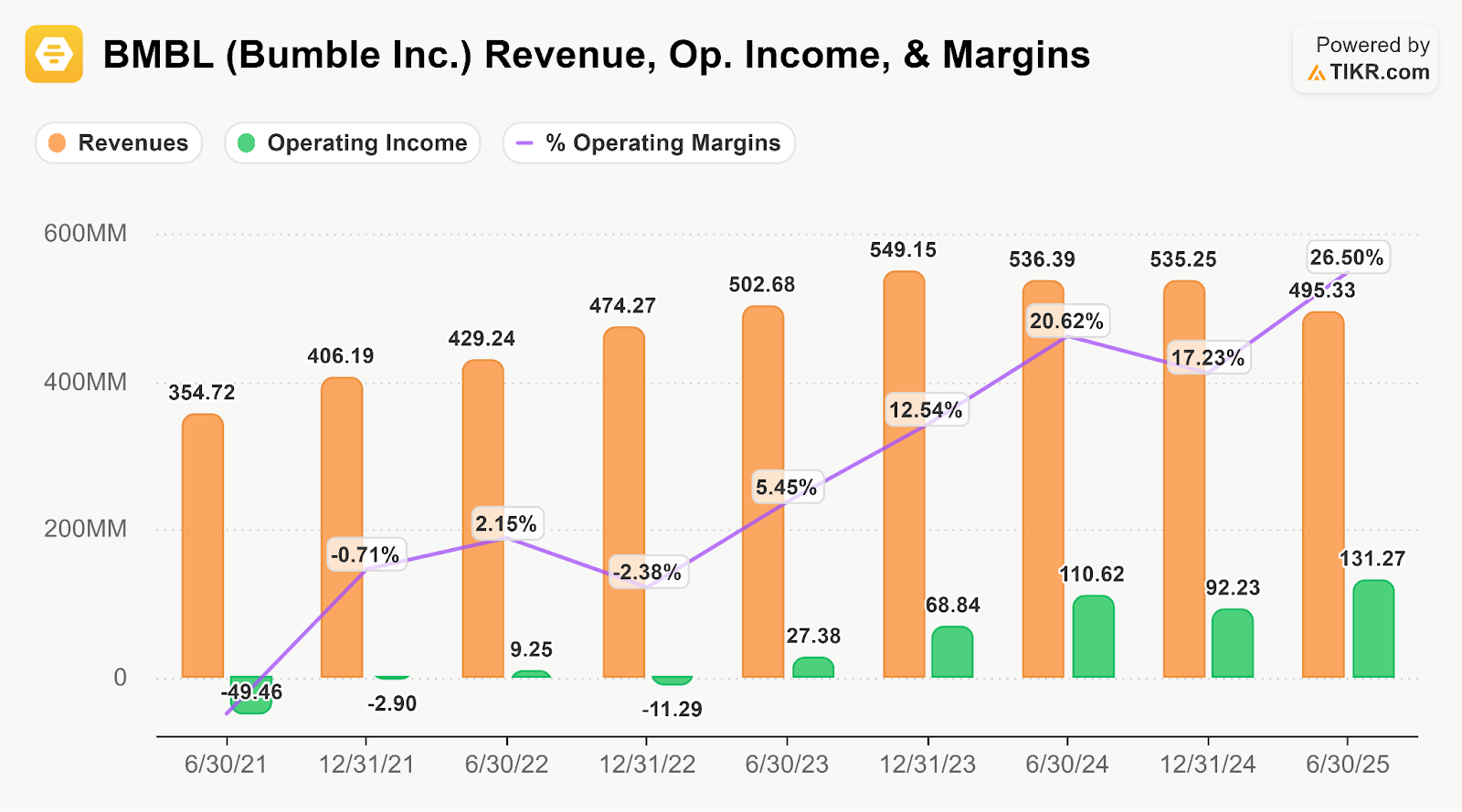

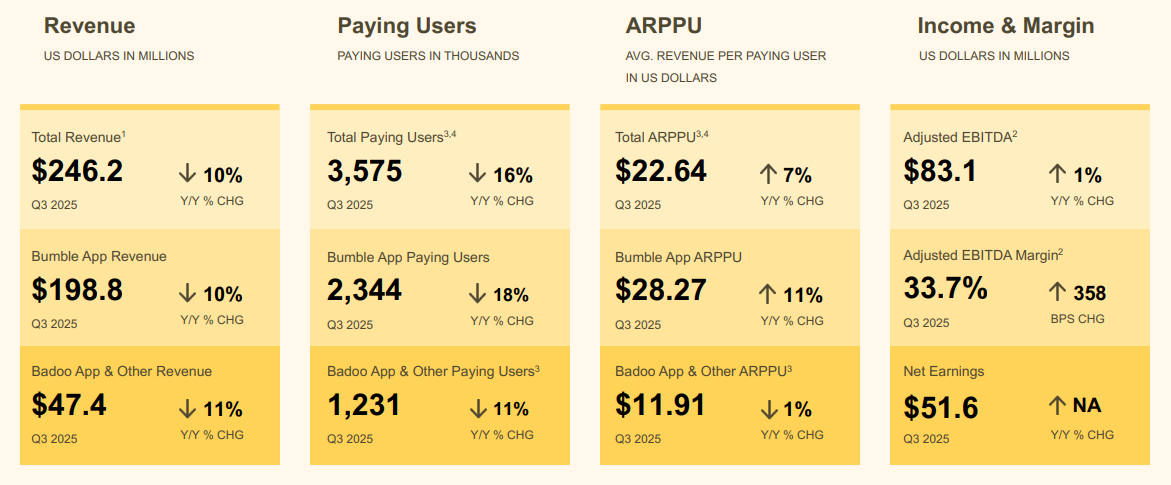

Bumble has pretty good geographic diversification, in the first 9 months of 2025 55% of total revenue came from outside the US. Despite what the share price chart suggests the underlying business has markedly improved from its IPO. They now make more in operating income in 3 months than they made in the first 3 years that followed their IPO.

Heterosexual dating apps are effectively a duopoly, if you want to find a wife from the comfort of your iPhone you are either paying Match or Bumble. Sure they each own smaller stand-alone apps like Hinge and Badoo that give the illusion of choice but the pricing power is firmly controlled by these two companies. This concentration combined with the value proposition of finding a wife (or at least a date to your cousin’s wedding) provides these firms tremendous pricing power and healthy operating margins.

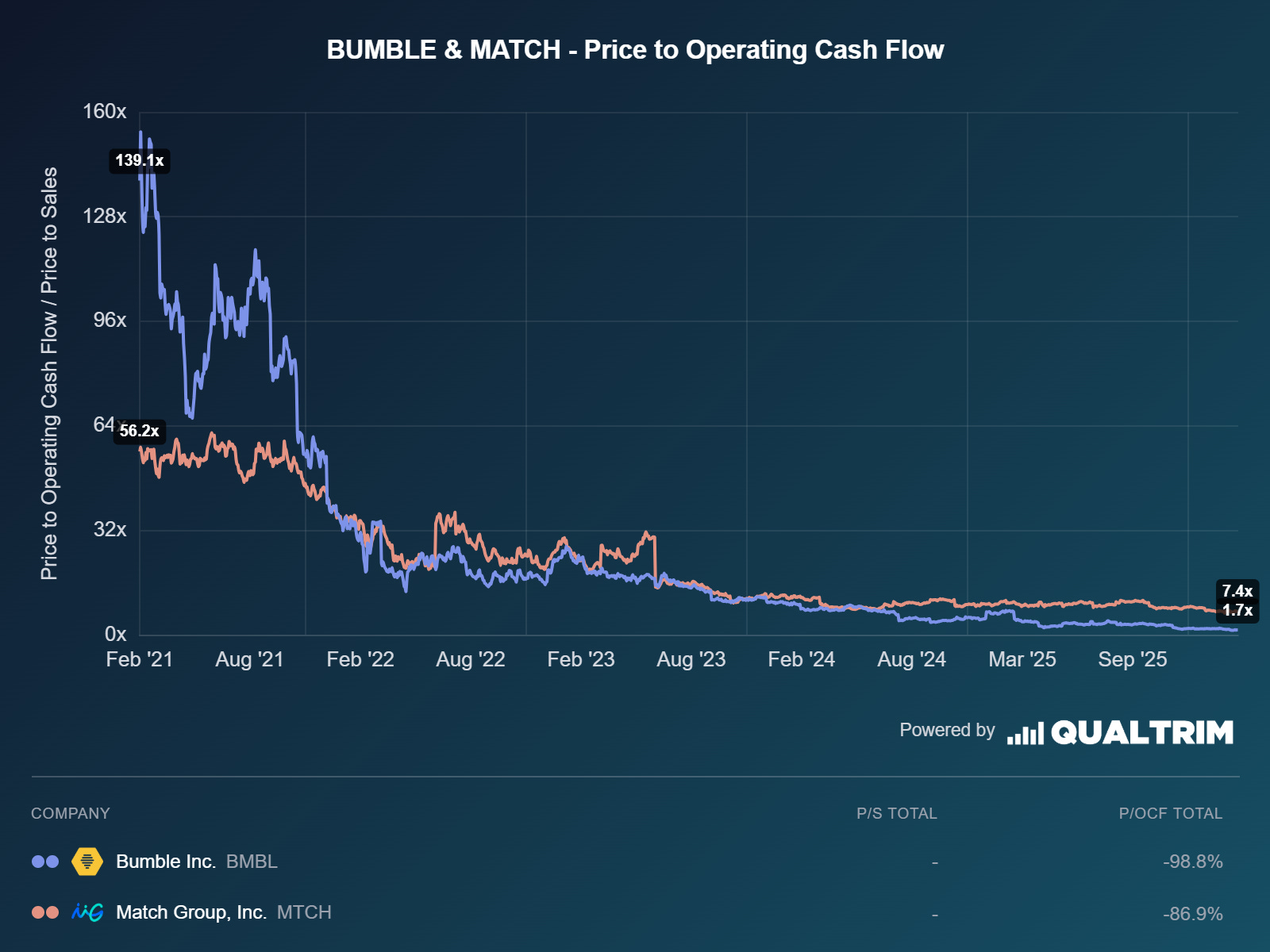

Investors were excited to pay a premium for this pricing power during the fervor of Bumbles IPO, inexplicably pricing the company at more than 100x its forward operating income. Today the dating software industry multiples have cratered and both trade close to all time lows. Even the investor darling Grindr has fallen out of favor with investors and is testing healthy but historical lows relative to their operating income.

Stock prices generally perform poorly during a 98.8% multiple contraction. Be aware the above figures for Bumble do not reflect the true share count and as such the market cap in the numerator is understated. The correct ending P/OCF multiple for Bumble is 2.2x and similarly the proceeding BMBL multiples are understated at an inconsistent ratio but the trend is clear. The business didn’t fail, rather investors failed to accurately evaluate it and until recently overpaid quite severely.

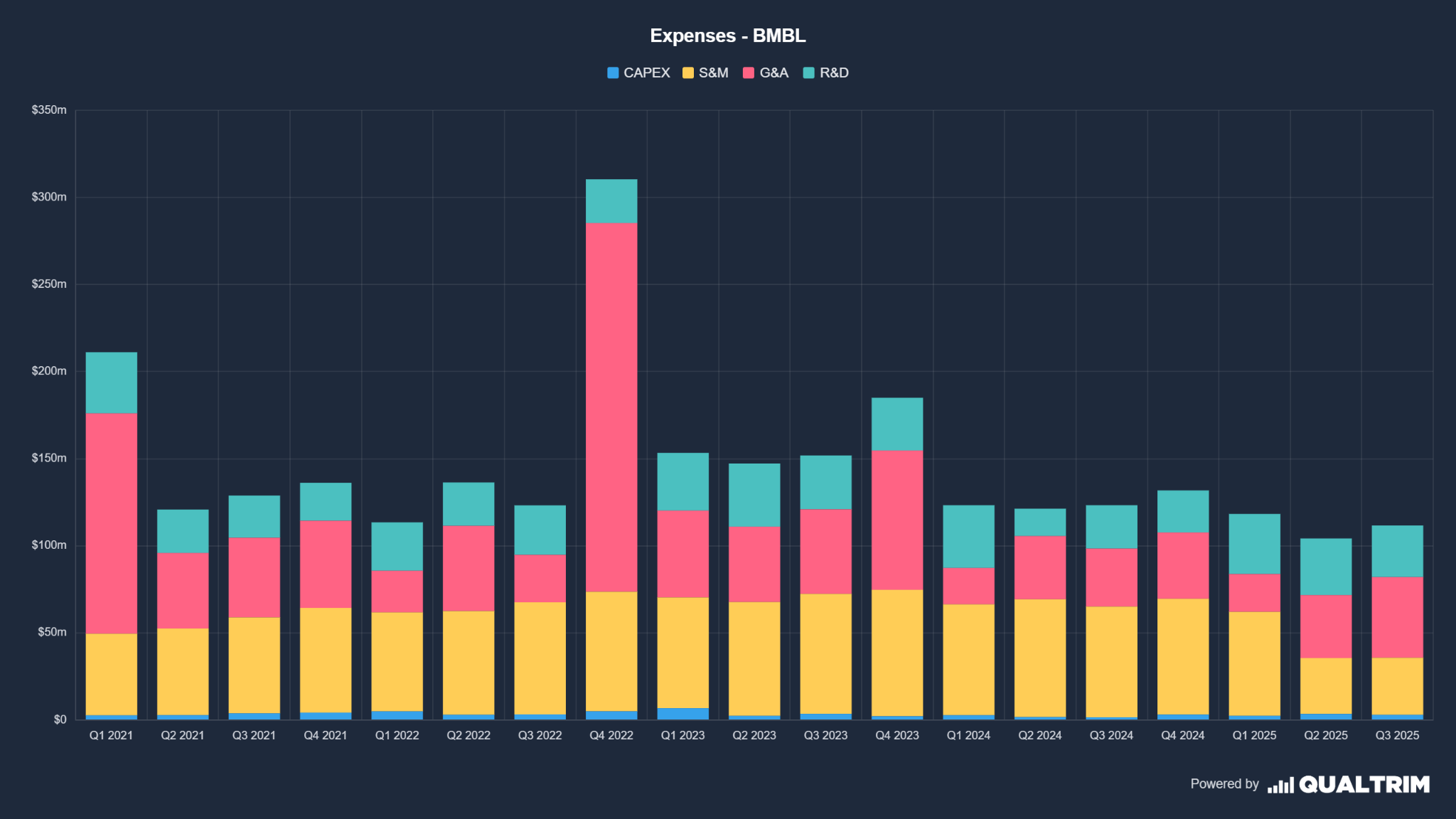

Bumble is in the midst of a house cleaning. They are attempting to prune bad actors, and emerge with a cleaner better product and pool of genuine profiles that people will be more prone to pay for. We can see some evidence to their success in the slight uptick in ARPPU in the face of a shrinking userbase. That’s not to say Bumble is in cigar butt mode, in fact the marketing spend pause initiated earlier in 2025 has partially resumed in Q4 and is showing promise that 2026 will be a return to growth.

The current performance marketing strategy has begun to show encouraging results with targeted audiences, attracting more approved-ready members into the ecosystem. While marketing spend is not expected to return to pre-transformation levels as we are focused on efficiency, we do expect some spend to return moving forward.

-CFO Kevin Cook (Q3 2025 November 6th)

This return to marketing uplift will be counteracted in Q4 by the effect of the trust and safety measures they began in August targeting bots, perverts, catfish, and other bad actors. They didn’t give an idea of the scale of this targeted account pruning but its possible Q4 paying user decline is more significant YOY than we saw in Q3 despite the uptick in ad spend. This is the cost of cleaning house and management is betting these improvements to their dating pool are worth the friction of their expanded mandatory verification measures.

“As Whitney has explained, we are committed to improving member base quality, and we expected these updates to result in increased attrition of targeted member segments over the near-term. That attrition is reflected in our monthly active user counts with the associated reduction in paying users creating a headwind to revenue this quarter. Since the trust and safety rollout occurred fairly late in the 3rd quarter, results for Q4 will reflect a comparatively larger full quarter impact, both from a paying user count and revenue perspective.”

-Former CFO Anu Subramanian (Q3 2023 November 7th)

In the interim KPI’s are falling and Bumble hemorrhaged 18% of their paying users in Q3 2025 compared to the year ago period. It’s not all bad news as lapsed users, while a worrying sign, must simultaneously be valued as an asset of sorts. The cost per install for new users is 4x higher than the cost to retarget return users and the conversion rate for return users to payers is 50% higher. Inactive users are a valuable pool and yet people tend to overvalue software with growing users and undervalue legacy software. This ignores the favorable economic advantage of retaining and retargeting users.

Dating in the AI Era & Surviving the SaaSpocalypse

Software companies are experiencing major selloffs as they face questions over long term viability. Decades of software iteration can now be replicated reasonably well by a Claude prompt in an afternoon. Bumble’s value lies not in its code base but its critical mass of users, particularly women as it maintains a higher percentage of women than both tinder and hinge. Furthermore the free offerings from Bumble, tinder, and hinge are tough to compete with which makes amassing a formidable user base marketing intensive and thus prohibitively expensive for any upstart competitors. The moat certainly appears to be shrinking for everyone in the cloud software subscription business but I think the incumbent dating apps are better positioned than most. Priced near 2x forward free cash flow anything short of immediate miserable failure should amount to a win for stockholders at current levels.

Bumble is planning a mid-year launch of their new Bumble cloud platform which they claim will allow for more nimble feature updates, fixes, and fine tuning aided by AI assisted user insights. They also plan to launch a standalone AI app, the R&D cost of which have already largely been paid for.

While their acquisitions have been duds, 2 of their 3 acquisitions were shuttered within 3 years, their internally developed app BFF (bolstered by their $10M acquisition of Geneva) has fared better. While BFF is not a revenue driver yet, the tepid success of their internally developed apps bodes well for their standalone AI app and provides potential for diversified avenues of growth.

“With minimal investment, BFF is already a top friend-finding app in the United States, especially among Gen Z and younger millennial women, and we see it as one of our most exciting long-term growth opportunities”

-Whitney Wolfe Herd (Q2 2025 Earnings Call)

AI has a real use case in automating matchmaking services, picking a partner based on proximity and a photo might not be the best way to skin a cat. We’ll see if the Bumble team have designed a better mousetrap later this year.

CEO & Management - Solid Operators & Lousy Allocators

In June Bumble laid off nearly one third of their workforce. The move is estimated to save them 40M a year, with severance and one time reorganization expenses this benefit largely won’t be recognized until Q1 2026. The knock-on effect for shareholders should be lower annual dilution from SBC. Historically, Bumbles SBC has been excessive in excess of 100M in both 2022 and 2023, due in part to the vesting of pre-IPO options and share class obligations. Stock based compensation was pared down to $25M in 2024 thanks to headcount reductions but it’s growing again. The return of founder Whitney Wolfe Herd as CEO after a 14-month hiatus came with a price tag. She was awarded $9M in SBC and her new CFO was handed $12M. You don’t become the youngest self made female billionaire by not looking out for yourself.

Their sign-on bonuses alone consumed more than half of what they saved by firing 30% of their workforce. Cutting 240 jobs to pay yourself a bigger bonus is not what I’d call moral management. Most people who take a sabbatical aren’t given $9M in equity upon their return. Just because obscene executive compensation is common doesn’t mean it needs to be common in the companies you invest in. Stock based compensation is the silent killer and it need to be monitored closely here.

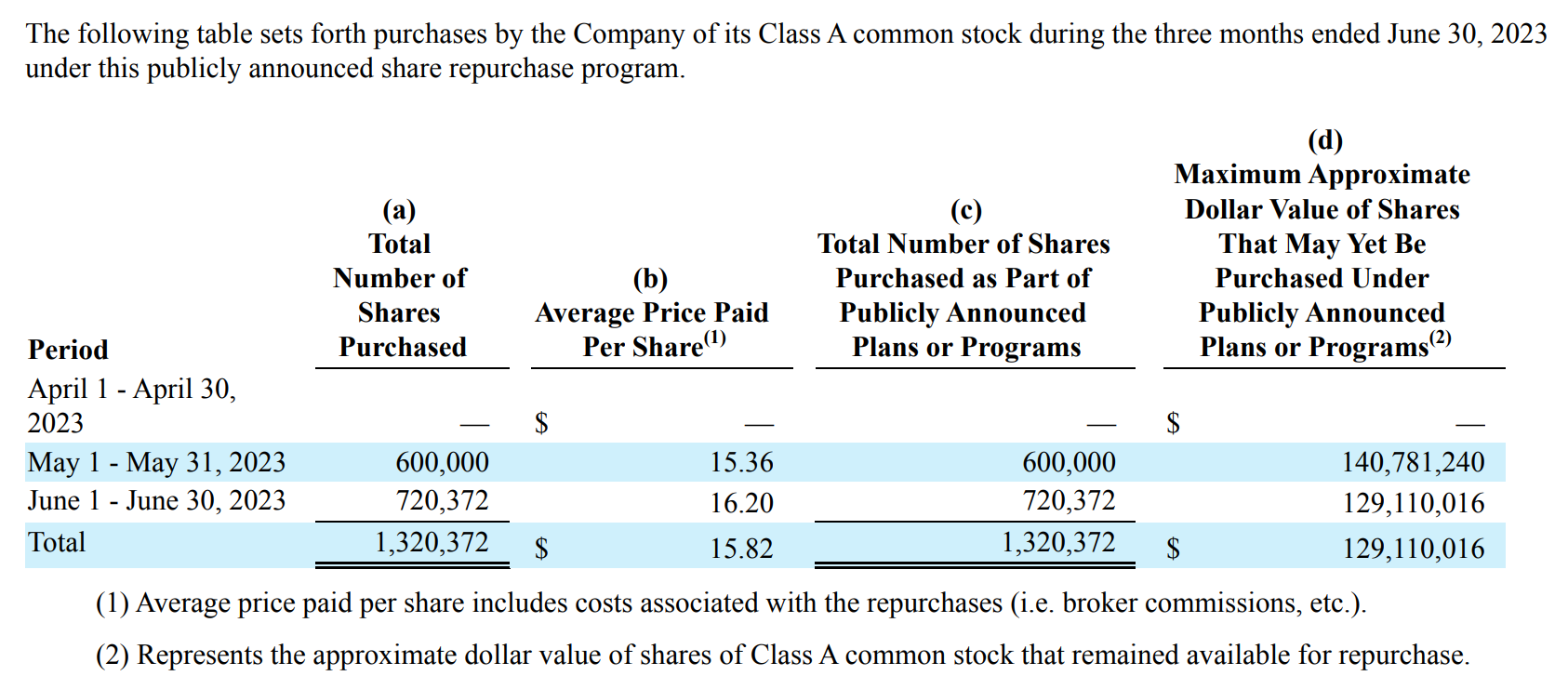

The biggest risk of value destruction isn’t typically executive compensation but rather capital allocation - particularly the price at which businesses repurchase shares and make dilutive acquisitions. Despite the sky high valuations bumble reached, the highest price they ever paid to repurchase shares was $16.20 per share in 2023.

With the benefit of hindsight their most expensive buyback looks like an overpayment but given their presumably rosier internal outlook at the time it certainly isn’t egregious. My own DCF calculations put fair value today within striking distance at $15.80. Given that the share price traded as high as $78.89, staying above $50 for most of 2021, it’s encouraging that they never repurchased shares at those inflated prices. Subsequent share repurchases of $379.3M from Q3 2023 to Q3 2025 averaged $9.14 per share, retiring another 41.5M shares. In total $400.2M was spent on share repurchases and 50.1M was left in their buy back program heading into Q4 2025. While Bumble investors may have been swept up in the IPO pandemic fervor, senior management showed they don’t simply repurchase shares at any price. I wouldn’t be surprised if they exhausted their 50.1M buyback program in Q4 and repurchased 7-8% of the remaining 150.5M in shares/common units.

Managements track record of acquisitions is decidedly less defensible. They have demonstrated an inability to identify accretive M&A opportunities, their most significant acquisition was a French dating app called Fruitz, Bumble paid $69.7M for the quirky European app and then sunset it within 3 years. They did the same thing with their second acquisition, a $9.8M couples communication app called Official. Their third, and most recent acquisition, Geneva was a $17.5 million community and group activities app that was rolled into BFF - expanding the app from a one on one friend finder to a more robust offering.

The good news is the massive market leader Match group fills much the same role that Jupiter does in our solar system protecting earth by absorbing smaller comets that might otherwise hit us. By purchasing most of the smaller competitors in the dating space they keep the dating app price war a friendly one vs one affair between Bumble and Match. They have probably saved Bumble from overpaying for a bad dating app or two through their aggressive M&A consolidation efforts which include over a dozen companies in the last 15 years.

Fair Value and Risks

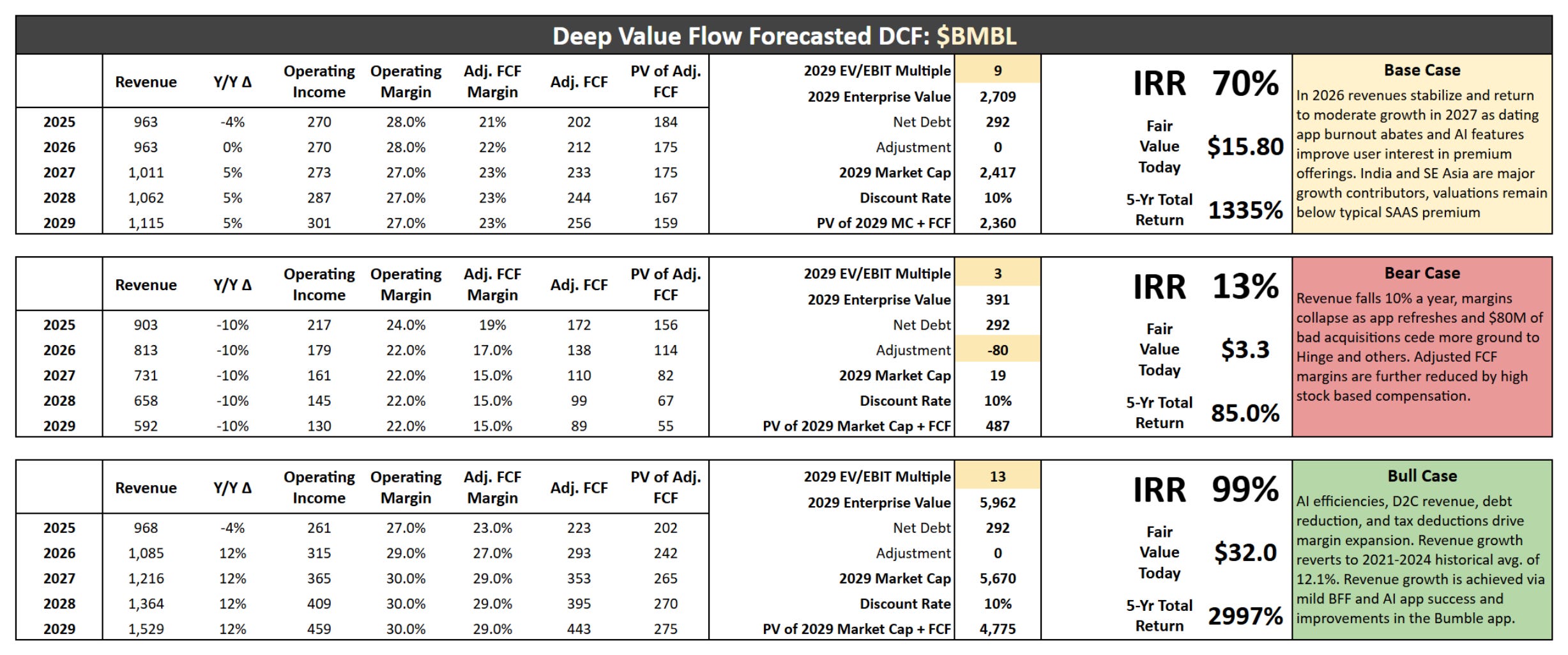

My thesis for Bumble is pretty simple: it’s a SAAS business trading near 2x cash flow which is insanity unless it’s about to implode, Bumble isn’t about to implode. The hidden tax asset is worth the price of admission here - if they maintain the current level of profitability the tax asset is worth more than the market cap of the company. Bumble has a decade of tax free earnings ahead making them a prime acquisition target. The bargain priced purchase of their tax receivables agreement has massively increased their expected cash flows which are already at all time highs.

I modeled what I believe to be three reasonable scenarios for future cash flows and I found it difficult to calculate a future in which Bumble achieves an IRR below 10% at the current share prices of $3.02 (Market Cap of 454.5M). Five straight years of double digit declining revenue paired with a significant margin collapse and $80M of lousy acquisitions still lead to cumulative adjusted free cash flow of $607M and a return likely to beat the market.

I believe fair value today conservatively sits near $15.80 per share. None of my base case assumptions to achieve this are particularly heroic. A return to moderate 5% revenue growth following 2 years of stagnation and a 9x EV/EBIT terminal multiple imply a future share price of $43.48 and a $6.5B market cap by 2031. Even at that blistering 70% IRR it’s well below the 7.7B market cap it achieved the day of it’s IPO.

I believe Bumble can sustain high margins of adjusted free cash flow even as they grow headcounts and return to marketing spend. On top of their tax shield, TRA elimination, and the rapidity at which they can reduce debt/interest they have a large lever they can pull with direct to consumer billing. Bumble has just scratched the surface of D2C revenue. As a result of Epic Games lawsuits against Apple and Alphabet app stores cannot gatekeep off-platform transactions and direct billing; as a result Bumble and others can move a significant percentage of large payments to their website and save 27% in fees. A double digit margin expansion across all businesses that rely on mobile app store revenue is underway.

“Direct billing tests continue to progress and nearly all members in the U.S. now have some form of direct billing available. We expect to refine our direct billing offerings in Q4”

CFO Kevin Cook (Q3 2025 Earnings Call - November 5th)

If Bumble moves a quarter of their 1B in revenue off platform by promising 10% discounts that’s an extra $42.5M per year hitting their bottom line (tax free for the next decade).

This company has problems; it’s not the industry leader, users are in decline, they have expensive debt, ARPPU has been flat over 5 years up just 2.5% from its average of $22.10, they have a terrible M&A track record, their largest shareholder Blackstone is exiting: already selling over $100M in stock for $6.26 per share, and the business maintains a tax structure and identity-based voting terms that gives Amber Wolfe Herd preferential treatment and 10:1 voting control until it sunsets on February 16th, 2028. Any one of those factors may send this to the no pile for most investors but in my estimation it doesn’t justify this rock bottom valuation given their tax assets, tailwinds, and price to prospective cash flows.

I’m long BMBL and a repeat college dropout, not your financial advisor. This is opinion/entertainment, not investment advice. Do your own research; you can lose money. I may buy/sell anytime without notice. No compensation from any company mentioned. Position Initiated February 2026; avg cost ≈ $2.79

This is one of my favorite write-ups. Bumble should frame your quotes in their office in bee-yellow: "Cutting 240 jobs to pay yourself a bigger bonus is not what I’d call moral management." "Most people who take a sabbatical aren’t given $9M in equity upon their return." Do you really think Bumble's tax assets are worth $247.5M? Bumble will not pay zero tax going forward. It will pay 15% or 12.6% due to OECD's Pillar Two treatment and Side by Side safe harbor, regardless of any tax assets. Bumble paid cash taxes of $18M and $29M in 2024 and 2025 (income tax provision - deferred income tax from CFO). This supports that Bumble will not be tax-free going forward. Assuming that Bumble can save 8.4% in tax (21% - 12.6%), and Bumble income is $145M, 11 years, that's only $134M. Much less than $247.5M. Did Blackstone and Whitney self-deal and sell this uncertain future benefit at the expense of shareholders? I don't know. "You don’t become the youngest self made female billionaire by not looking out for yourself." I'd rather they collect the benefit in the future, together with the rest of the shareholders. Want to know your thoughts about the hidden tax assets. Still an interesting opportunity, though. By the way, AI said that the $186 million payment serves as a "complete and full termination" of all of Bumble's payment obligations, explicitly covering past, current, and future obligations.

Impressive timing